Summary of this article:As long as you are an entity that engages in commercial activities, not minding your rank on the supply chain, you would always need to understand how to calculate the cost of goods you purchase. Understanding your very own figures helps you know the total cost of your inventory, prepare financial statements, estimate and analyse what your profit margin could look like and create a balanced comprehension of your purchasing activity during an accounting period. As commercial activities enhance world living standards, it will be essential for merchants to fully grasp the difference between "The cost of goods purchased" and "The cost of goods sold". They may sound the same, but they are not the same. The cost of goods purchased refers to the total cost of all inventory procured, while the cost of goods sold refers to the total cost of goods or inventory cost, actually sold out to customers during that same period. This article will explain what is implied when a statement like "The cost of goods purchased" is mentioned, why it is of utmost importance, the formula used to calculating it and how businesses should practice it accurately in their daily dealings.

What Is Meant By The Cost Of Goods Purchased?

The cost of goods purchased is the total amount of money a business spends on inventory and stock during an accounting period, calculated alongside all purchase-related items such as freight-in, purchase returns, allowances and discounts.

The importance of the cost of goods purchased is usually mainly needed by merchandising businesses that purchase finished products for resale purposes. The reason why this information would be useful to merchants instead of manufacturers would be because these businesses do not produce inventory by themselves. Instead, they procure goods from suppliers and then sell them to consumers.

Good examples of businesses that calculate the cost of goods purchased include:

● Retailers/ Retail stores.

● Online sellers.

● Wholesalers.

● Distributors.

● Import-export traders.

This evaluation shows how much inventory was procured in a certain period of time and not how much inventory was sold.

What Makes Evaluating The Cost Of Goods Purchased Important?

Evaluating the cost of goods purchased can help businesses in the following ways:

● Keep an eye on inventory buying activities.

● Carry out financial statement activities accurately.

● Make calculations on cost of goods sold accurately.

● Continuously assess supplier spending.

● Enhance budgeting and purchasing work flow control.

● Understand the flow of inventory over time.

If any of the figures are wrong, it will affect the gross profit, the inventory evaluation and the overall financial reporting negatively.

The Cost Of Goods Purchased (The Formula)

The standard formula is:

Cost of Goods Purchased = Total Purchases + Freight-In - Purchase Returns and Allowances - Purchase Discounts

This formula will help you come up with the net cost of inventory bought during the accounting period.

Let’s break down each segment of this formula.

Total Purchases

The total purchase amount is the total amount spent on buying inventory before adjustments. It includes the cost of all goods purchased for resale during a certain period.

Freight-In

Freight-in refers to the shipping or transportation costs incured and settled (paid) by the buyer to get purchased inventory to the business location, warehouse or fulfillment center. These costs cannot be removed from the inventory cost and so should be added.

Purchase Returns and Allowances

If the buyer sends already purchased products back to the supplier or receives a price reduction because of defective, damaged or other issues, these amounts reduce the total cost of purchases and have to be subtracted from the total cost of goods purchased.

Purchase Discounts

If the supplier offers an early payment discount or any other type of purchase discount, the amount should also be deducted from the total cost of purchases.

Basic Examples Of "The Cost Of Goods Purchased"

Assuming a business has the following figures for one month:

● Total amount spent on purchases: $50,000

● Freight-in: $2,000

● Returns/allowances deducted for defective or faulty goods: $3,000

● Purchase discounts granted by suppliers: $1,000

Using the formula:

Cost of Goods Purchased = $50,000 + $2,000 - $3,000 - $1,000

Cost of Goods Purchased = $48,000

This would mean that the company purchased inventory worth $48,000 during that month on a net basis.

How The Cost Of Goods Purchased Differs From The Cost Of Goods Sold

This is one of the most important distinctions in accounting.

Cost of Goods Purchased

This shows the total amount which was spent on inventory during a particular period.

Cost of Goods Sold

This shows how much inventory cost was actually sold out to customers during the same period.

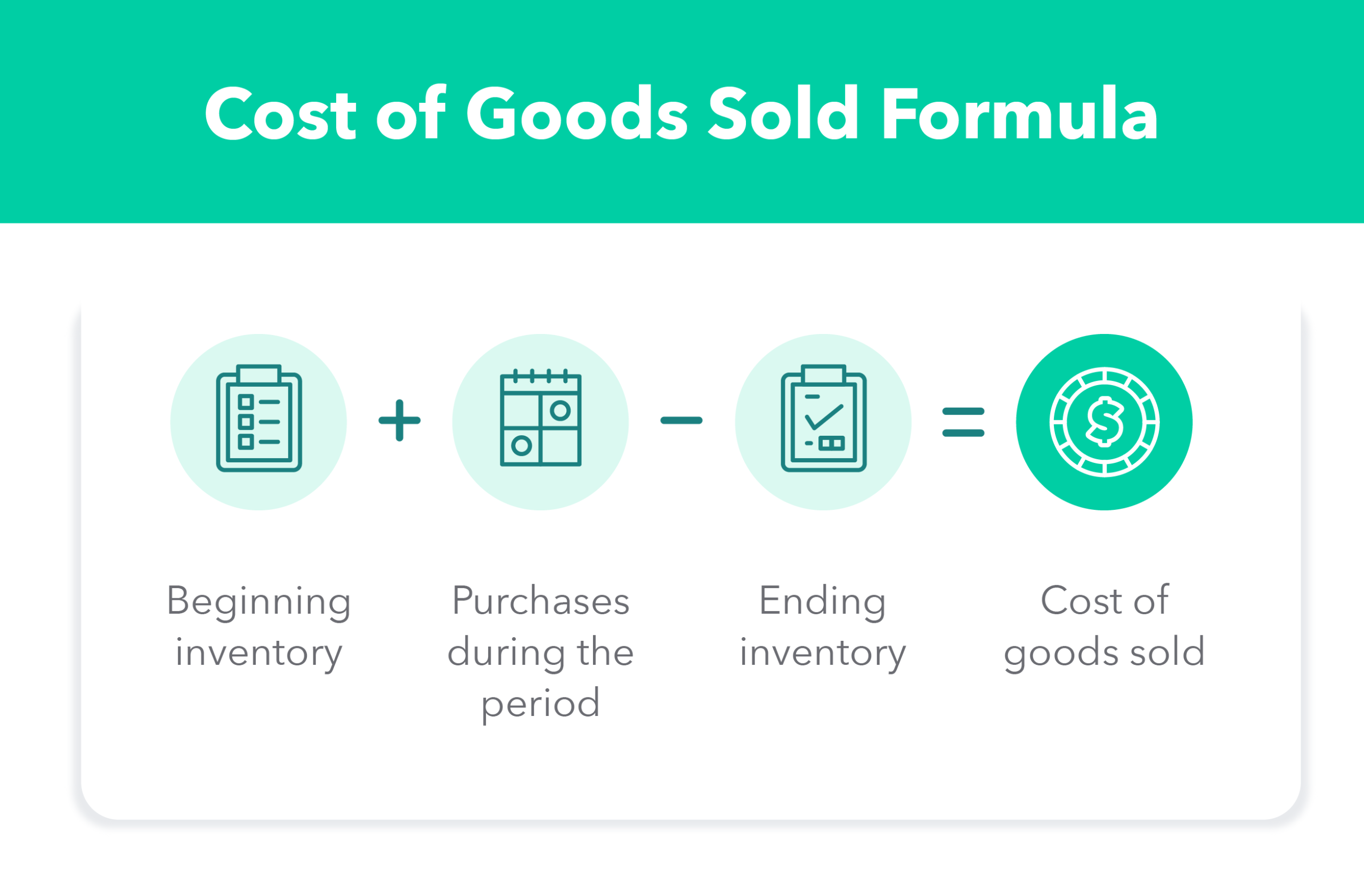

The formula for cost of goods sold is:

Cost of Goods Sold = Beginning Inventory + Cost of Goods Purchased - Ending Inventory

So cost of goods purchased is often one step in calculating cost of goods sold.

A Full Example Of Evaluating Cost of Goods Sold

Let’s say a business has:

● Opening year inventory (Beginning inventory) : $20,000

● Total cost of purchases: $60,000

● Freight-in: $4,000

● Returns/allowances on defective goods: $2,000

● Supplier granted discounts: $1,000

● Closing year inventory (Ending inventory) : $25,000

Step 1: Evaluate Cost Of Goods Purchased

Amount spent on Goods Purchased = $60,000 + $4,000 - $2,000 - $1,000

Actual cost of Goods Purchased = $61,000

Step 2: Evaluate Cost Of Goods Sold

Amount spent on Goods Sold = $20,000 + $61,000 - $25,000

Actual cost of Goods Sold = $56,000

In this example, the business purchased $61,000 worth of inventory during this period, but then only $56,000 became cost of goods sold.

Formula In A Periodic Inventory System

The cost of goods purchased formula is mostly used in periodic inventory systems. In this type of systems, businesses update stock records at the end of the accounts year rather than after every sale or purchase.

In a periodic system, purchases are tracked in a separate purchases account and the business calculates:

● The net purchases.

● The actual cost of goods purchased.

● The actual cost of goods available for sale.

● The actual cost of goods sold.

This makes the cost of goods purchased an important part of the periodic-end accounting.

Formula in a Perpetual Inventory System

In a perpetual inventory system, stock records are continuously updated. Every purchase is directly recorded in the inventory bookkeeping accounts and each sale reduces inventory and keeps account of the cost of goods sold in real time.

Even in a perpetual system, businesses may still assess the cost of goods procred over a period for proper accontability, reporting and analysis. However, the cost of goods purchased is more commonly emphasized upon in the periodic functional system.

Items Included In The Cost Of Goods Purchased

To evaluate these figures correctly, businesses need to include only costs directly related to inventory prchased for resale.

Such items would usually be:

● Inventory purchased for resale.

● Import duties incurred due to inventory shipment.

● Non-refundable taxes on procured goods.

● Freight and final destination delivery costs.

● All costs directly tied to getting inventory to its final consumer.

All these costs fall into amounts incurred when procuring inventory and should be included into inventory cost where need be.

Items Not Included In The Cost Of Goods Purchased

There are certain expenses that need not be included into the cost of goods purchased because they are operating expenses and not inventory purchase costs.

Examples include:

● Expenses incurred in the sales process.

● Advertisement expenses.

● office rent.

● Staff salaries.

● Costs of storing goods after reception (unless needed for production or acquisition.)

● Extra shipping delivery to individual customers.

● Regular business travel expenses.

Including expenses not included in the cost of direct purchases will inflate inventory cost and distort financial recording.

How To Calculate The Cost Of Goods Purchased Step by Step

Here is a simple step-by-step process.

Step 1: Identify Total Inventory Purchases

Add up all cost incurred through inventory procurement during the accounting period. To better get accurate figures, use supplier invoices, purchasing records and inventory reports.

Step 2: Add Freight-In and Direct Acquisition Costs

Add up transport related charges incurred in bringing goods to its final destination or target market.

Step 3: Subtract Returns and Allowances

Deduct the value figure of goods returned to the supplier because of defects or shortages and discounts granted by supplier still due to defects or shortages.

Step 4: Subtract Purchase Discounts

Should the supplier give you any discounts due to bulk buying, please deduct them from total purchases.

Step 5: Confirm The Final Net Amount

The result gotten from the summation of the cost of direct purchases mins the total amount which comes from product returns and discounts is your cost of goods purchased for the period.

Practical Example for an E-Commerce Business

An online seller imports household products from an overseas supplier. During one quarter, the business records:

● Products procured: $80,000

● Sea freight and inland delivery: $6,500

● Import custom duties: $2,000

● Faulty/defective returns: $4,000

● Supplier discount: $1,500

Calculation:

Cost of Goods Purchased = $80,000 + $6,500 + $2,000 - $4,000 - $1,500

Cost of Goods Purchased = $83,000

This means the commercial entity acquired $83,000 worth of inventory during the quarter.

Common Mistakes When Calculating The Cost of Goods Purchased

Businesses often make avoidable errors when preparing this number.

Confusing Purchases with Cost of Goods Sold

Some business owners often like to believe that everything purchased during the month will be sold during that same month. This is not always the case. Unsold products procured remain as assets and not expenses.

Ignoring Freight-In

The inbound shipping cost is and should be considered as part of the inventory acquisition cost.Though most business entities often leave it out, leaving it out underestimates the true purchase cost.

Forgetting Returns and Discounts

Failing to deduct discounts and defective product reimbursements or discounts could cause cost of goods purchased figres to be higher than normal. This is a common mistake that most business entities make.

Including Operating Expenses

Another mistake which is very common is including other business expenses not partaining to the goods procurement into the calculation. Only inventory-related procurement costs belong to this calculation. General business expenses should not be added when calculating the cost of goods purchased.

Poor Recordkeeping

Some businesses are careless with bookkeeping which makes it difficult to calculate purchases accurately. Price invoices, freight bills, taxation documents and supplier credit notes should all be properly preserved to help with accurate purchase cost calculations.

How Cost of Goods Purchased Appears in Financial Reporting

For most business entities using periodic business systems, the cost of goods purchased helps in the calculation of the cost of goods ready and available for sale and also helps in the calculation of the cost of goods sold.

The sequence is usually:

1. Opening inventory.

2. Include the addition of the: Net purchases or cost of goods purchased.

3. Equals: cost of goods ready for sale.

4. Less: Closing inventory.

5. Equals: Cost of goods sold.

This shows that the cost of goods procured is not always seen as a final line item on the income statement but it is a key internal accounting and financial statement figure.

Tips To Improve Upon Accuracy

To be able to execute accurate calculations correctly and consistently, businesses should:

● Always differentiate between inventory purchases and operation expenses.

● Always keep clear track of the inbound freight.

● Keep accurate record of supplier credit notes promptly.

● Ensure purchase records and inventory movements are always the same,coherent and consistent.

● Assess discounts and payment functional agreements consistently and carefully.

● When ever you are dealing with international purchases, ensure customs and import cost records are properly kept for proper financial book keeping.

● Endeavor to make use of accounting softwares or inventory in/out flow data processing systems when possible.

Accurate calculations give room for better gross margin assessments and stronger financial control.

Conclusion

Mastering how to calculate the cost of goods purchased is of utmost importance. Having an indept grasp of inventory activities and maintaining accurately executed accounting records will always help you master your business figures while guiding you through making better and more efficient purchase decisions. The formula is easy to grap, but still, every detail matters. Businesses should add up only purchase-related costs and deduct returns, allowances and discounts to arrive at the correct figure.

The basic formula is:

Cost of Goods Purchased = Total Purchases + Freight-In - Purchase Returns and Allowances - Purchase Discounts

Once this number is calculated, it can be used to help determine cost of goods sold and support better inventory and financial management.

For retailers, wholesalers, importers and e-commerce sellers, mastering this calculation is a basic but essential part of running a healthy business.

FAQ

What is the formula for cost of goods purchased?

The formula is:

Cost of Goods Purchased = Total Purchases + Freight-In - Purchase Returns and Allowances - Purchase Discounts

Is the cost of goods purchased usually the same as the cost of goods sold?

No. The cost of goods purchased is the sum total of inventory bought during the period when all returns and allowances related to the purchase has been deducted. The Cost of goods sold is the total cost of inventory purchased minus the actual cost of inventory sold during the period.

Can I include the shipping cost when calculating the cost of goods purchased?

Yes, inbound shipping or freight cost associated with delivering inventory to final location is usually included.

Are supplier discounts included in cost of goods purchased?

Supplier discounts are deducted from the cost of purchases.

Who uses the cost of goods purchased calculation?

Retailers, wholesalers, distributors, trading companies and e-commerce businesses. It is commonly used to evaluate the cost of inventory purchases during an accounting period.